Category Archives: Captial Markets

US retreat from the Middle East opens the door to more Russian involvement and influence

A New World Order? Putin’s Russia, Syria, Iran, The Middle East and Oil..

On SeekingAlpha.com -The Peoples Bank of China Selling U.S. Treasuries Is Not ‘QT.’ Quite The Opposite…

Is ISIS a threat to Saudi Oil Fields?!

Kurdish Peshmerga move into Kirkuk countering Islamic extremist moving down from Mosul

Saudi Arabia, Iran and Oil prices

Crisis in Syria: Impact on regional oil exports

See my interview on CNBC with Brian Sullivan and Mandy Drury regarding the imminent US strike against Syria and potential impact on regional oil supplies. http://video.cnbc.com/gallery/?video=3000195128

The Fed – Getting Back to “Normal”

The Fed’s tapering should not be viewed as a reduction in their accommodative monetary policy; rather the Fed is anxious to return to a more normal posture in the financial markets and to regain flexibility of action to respond to future market panics. Historically (pre QE) an accommodative Fed position in the market would be reflected in a steep positive yield curve. A positive yield curve is made up of lower short term interest rates and higher long term rates. In an effort to rebuild the demand of a devastated housing market; the Fed, through QE, has forced the curve flatter during a period of monetary accommodation resulting in historically low mortgage rates. Recent data does argue that the Fed’s stimulus targeting housing has worked in spite of continued credit tightening by banks unwilling to lend. The current yield curve explains to a large extent bank’s hesitation to lend. Banks generally borrow short and lend long. A relatively flat yield curve does not create incentives for banks to lend because spreads are too narrow. Indeed the traditional response to a restrictive money policy is a flat yield curve as the Fed seeks to cool the economy by reducing credit. So, during this recent emergency move described as quantitative easing (QE), the Fed has been working at cross purposes by targeting retail demand for mortgage while reducing incentives for banks to lend. Continue reading

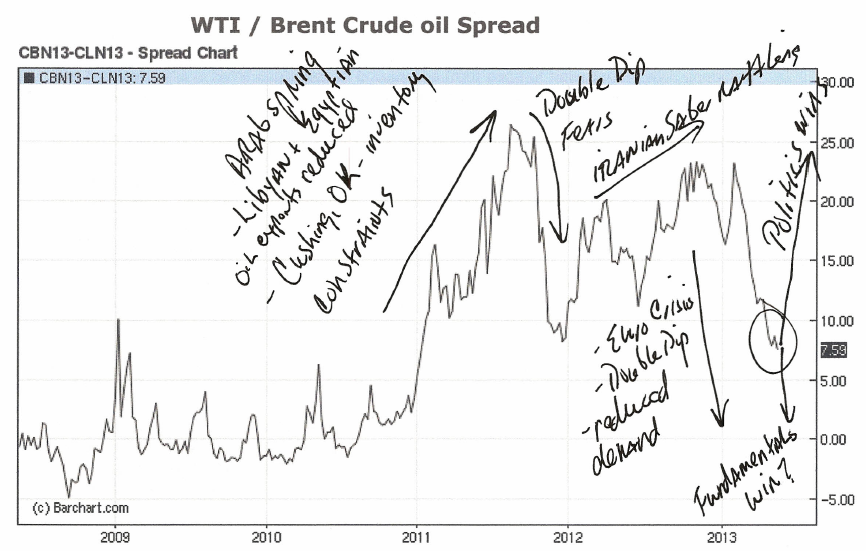

Brent/WTI Crude Oil Spread – Complacency or Just Fundamentals??

COMPLACENCY OR JUST FUNDAMENTALS??

- Greatest risk level since early 2011 to sudden spread widening due to real or perceived supply disruption/ headline risk.

- Supply/demand fundamentals continue to pressure the WTI/Brent spread lower towards the long term average of +/- $5.

- As North American production continues to increase and replace imported oil increasingly the WTI/Brent spread will reflect and be contained to Brent oil price swings.

- OPEC continues to reduce production, $90 per barrel price acceptable to OPEC and OPEC expects increase in demand from improving economies in the second half of the year. Continue reading